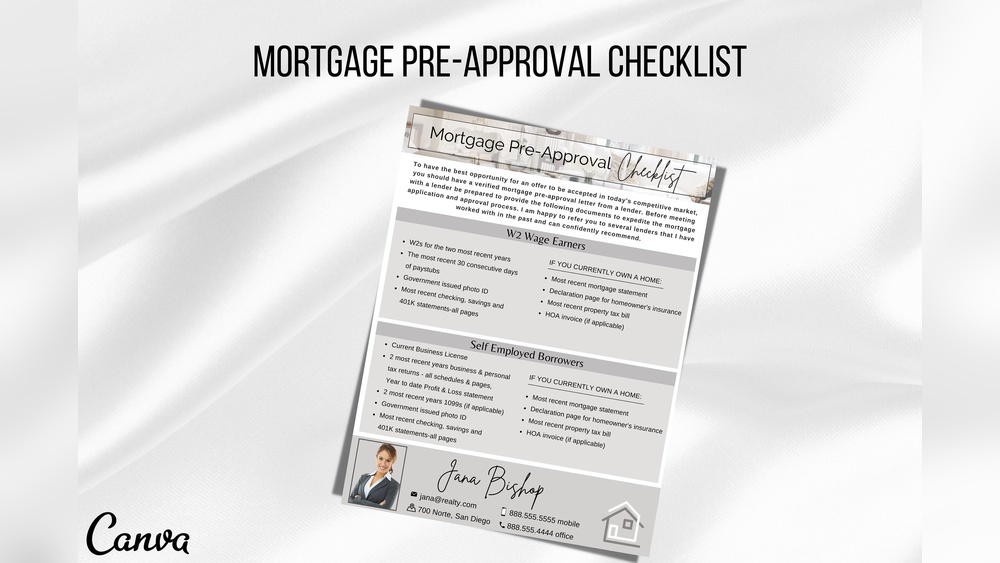

Getting approved by a mortgage lender can feel overwhelming, but knowing exactly what you need can make the process much smoother. If you want to secure the best loan and move into your dream home without delays, having a clear Mortgage Lender Approval Checklist is essential.

This checklist will guide you step-by-step through the key documents and information you must gather before applying. By preparing ahead, you’ll avoid last-minute stress and increase your chances of quick approval. Ready to take control of your mortgage application? Keep reading to discover the must-have items that will keep your approval on track.

Prepare Personal Identification

Government-issued ID is essential for mortgage approval. Lenders use it to confirm your identity. A valid driver’s license or passport works well.

The Social Security card verifies your Social Security number. This helps lenders check your credit and employment history.

Providing proof of residency shows where you live. Recent utility bills, lease agreements, or a mortgage statement can serve this purpose. These documents must have your name and current address.

Gather Income Documents

Recent pay stubs show your current income clearly. They help lenders confirm your earnings quickly. Tax returns provide a full record of your income over the past years. Lenders use them to check your financial stability and tax history.

W-2 forms show your yearly wages from employers. 1099 forms report income from freelance or contract work. Both forms help prove different income types clearly.

Self-employment records include profit and loss statements or bank statements. They are vital for self-employed borrowers to prove steady income.

| Document | Purpose |

|---|---|

| Recent pay stubs | Confirm current income |

| Tax returns | Verify overall income history |

| W-2 forms | Show yearly wages from employers |

| 1099 forms | Report freelance or contract income |

| Self-employment records | Prove income for self-employed |

Compile Asset Statements

Bank statements provide proof of your current funds. Lenders want to see consistent deposits and withdrawals. They check for large, unexplained transactions that might affect your loan.

Retirement accounts like 401(k) or IRAs show your long-term savings. These accounts can sometimes be used as assets for loan approval. Statements should include the account balance and recent activity.

Investment portfolios include stocks, bonds, and mutual funds. Lenders look at their value and stability. Provide detailed statements from your broker or financial institution to confirm your assets.

Verify Employment History

Employer contact details are essential for verifying your job status. Lenders need a phone number or email to confirm your work history. This helps them check your income and job stability.

An employment verification letter from your employer adds proof. It should state your job title, start date, and current salary. This letter must be on company letterhead and signed by a supervisor or HR representative.

Both documents help lenders trust your income claims. They reduce delays in the mortgage approval process. Keep these ready and updated for a smooth application.

Check Credit Information

Credit report review is a key step in mortgage approval. It shows your credit history and current debts. Lenders use this to decide loan eligibility.

Check the report for errors or outdated info. Fixing these can improve your score.

Address credit issues by paying down debts or disputing mistakes. Missing payments or high balances can lower your score.

Improving your credit report can make approval easier and may get you a better interest rate.

Document Property Details

Purchase agreement is a key document showing the home’s price and terms. It proves you have a deal with the seller. Lenders use this to confirm the loan amount and conditions.

Property appraisal is an official report by a licensed appraiser. It shows the home’s market value. This helps lenders decide if the property is worth the loan amount.

Homeowners insurance protects the home from damage or loss. Lenders require proof of insurance to ensure their investment is safe. This policy must be active before closing the loan.

Prepare Additional Documents

Gift fund letters prove the source of money given to you for the down payment. Lenders need these letters to confirm the funds are a gift, not a loan. The letter must state the amount, donor’s relationship, and that repayment is not required.

Divorce decrees show legal agreements from a divorce. They clarify who pays alimony or child support. This helps lenders understand your financial obligations and income. Providing the full decree avoids delays in loan processing.

Bankruptcy records reveal past financial problems. Lenders review these to assess risk. Include all paperwork showing discharge dates and details. This transparency helps lenders decide on your mortgage eligibility.

Organize Documents For Submission

Start by making a checklist of all necessary documents. Include proof of income, bank statements, tax returns, and ID. Organize these papers by category to avoid confusion. Keep the list handy for quick reference.

Scan each document clearly and save them as files on your computer. Use easy-to-access folders with clear names. This helps you find files fast when the lender asks. Digital copies are safer and easier to share than paper ones.

Check that all scanned files are readable and complete. Make backups on a USB drive or cloud storage. Keep your digital files updated if any new documents come in. This preparation speeds up your mortgage approval process.

Communicate With Your Lender

Respond quickly to any document requests from your lender. This helps keep the process moving smoothly. Always check your email and phone for messages. If you get a question, answer it right away.

Clear communication avoids delays. If something is unclear, ask your lender to explain. Don’t wait or guess. Fast and honest answers build trust and help your loan get approved faster.

Keeping all requested papers organized also helps. Have your pay stubs, bank statements, and ID ready. This shows you are prepared and serious about the loan.

Review Final Approval Steps

Review the loan estimate carefully. This document shows your loan costs, interest rates, and fees. Make sure all details match what you expect. Check the loan amount and monthly payment. Ask questions if numbers seem wrong or unclear.

Schedule your closing appointment early. Contact your lender or title company to set a date. Closing usually happens a few days before or on your move-in day. Bring all required documents, like ID and proof of insurance, to the appointment.

At closing, you will sign many papers. This makes the loan official and transfers the property to you. Prepare to pay closing costs, if not already paid. After signing, the lender will fund your loan, and you will get the keys.

Frequently Asked Questions

What Documents Are Needed For Mortgage Lender Approval?

You need proof of income, tax returns, bank statements, and ID. Lenders also require credit history and employment verification. Having these ready speeds up approval.

How Long Does Mortgage Lender Approval Take?

Approval usually takes 30 to 45 days. It depends on document completeness and lender workload. Promptly submitting requested papers can shorten this period.

Can I Get Approved With Bad Credit?

Approval is possible but challenging with bad credit. Higher interest rates or larger down payments may apply. Improving credit score before applying helps approval chances.

What Is A Mortgage Pre-approval Checklist?

It’s a list of documents lenders need before approving a loan. Includes pay stubs, tax returns, bank statements, and ID verification. Pre-approval shows sellers you’re a serious buyer.

Conclusion

Preparing all documents carefully speeds up mortgage approval. Keep your income, assets, and identification ready. Double-check every paper before submitting your application. Clear and complete files help lenders make quick decisions. Stay organized and respond promptly to any lender requests.

This checklist guides you to a smoother mortgage process. Taking these steps boosts your chances of approval. Start early and keep everything in one place. Your home loan journey becomes easier with good preparation.