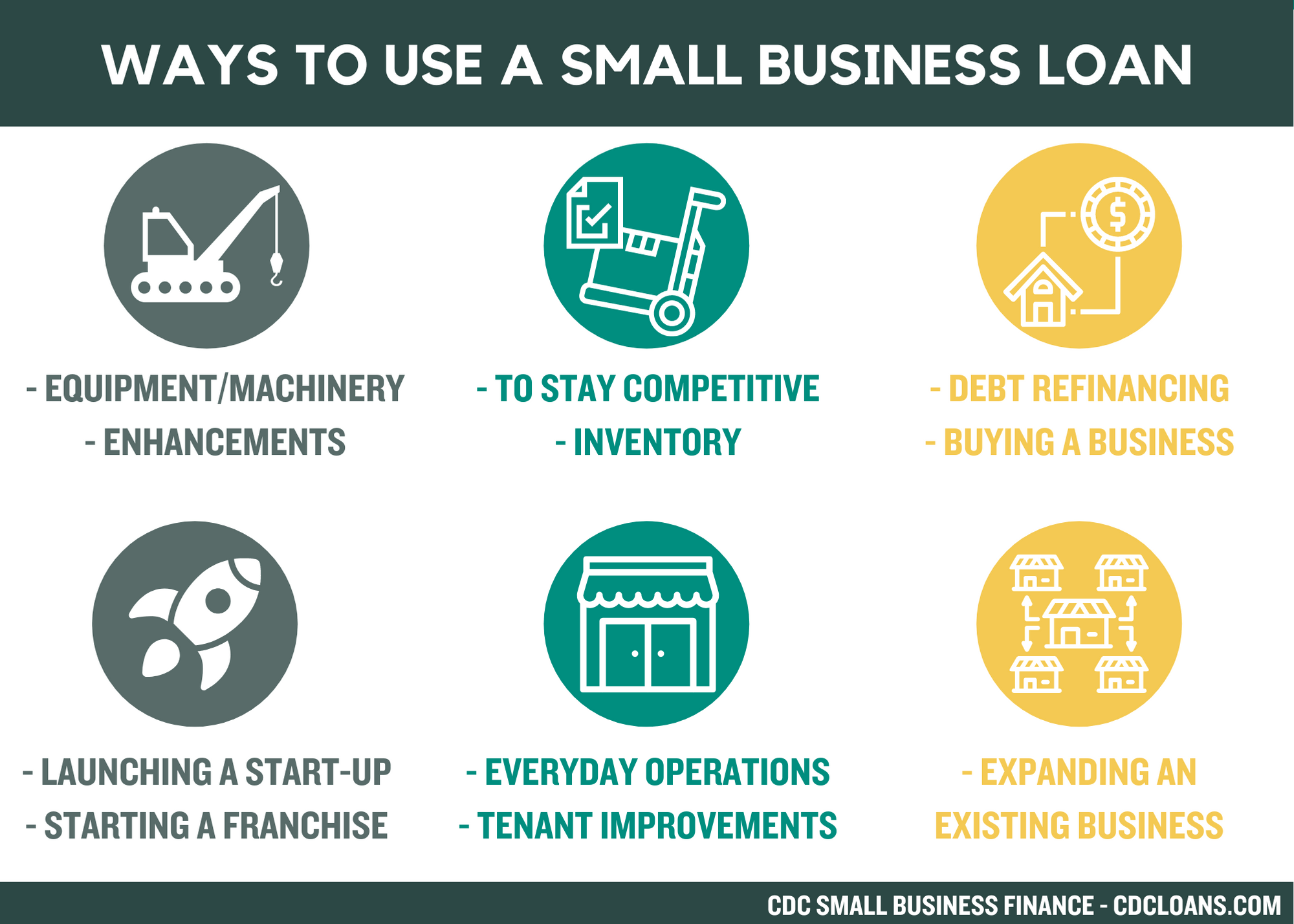

Thinking about starting your own franchise but unsure how to fund it? Finding the right loan lender can make all the difference in turning your dream into reality.

You want financing that fits your unique needs, offers reasonable terms, and supports your growth. But with so many franchise loan lender options out there, it’s easy to feel overwhelmed or stuck. This guide breaks down the top choices available to you, helping you understand which lenders match your goals and how to secure the best deal.

Keep reading to discover how to unlock the funding you need to build your franchise success story.

Franchisor Financing

Franchisor loans offer a direct way to fund your franchise. They often come with lower interest rates compared to other loans. Terms can be more flexible, which helps new franchisees manage payments. These loans may include support or training from the franchisor, adding value beyond money.

Choosing franchisor financing makes sense when banks deny your loan. It is also useful if you want faster approval and less paperwork. Franchisor loans are good for those who want to stay fully linked with the franchise brand. These loans help build trust between you and the franchisor, making future support easier to get.

Bank Loans For Franchises

Traditional bank loans offer a common way to fund franchises. These loans usually have fixed interest rates and set repayment terms. Banks prefer borrowers with a good credit score and stable income. They often ask for a detailed business plan and financial history. Collateral might be required to secure the loan.

| Qualifying Criteria | Description |

|---|---|

| Credit Score | Typically 650 or higher for better loan terms |

| Business Plan | Clear plan showing how the franchise will succeed |

| Collateral | Assets like property or equipment to secure the loan |

| Income Proof | Steady income to show ability to repay |

Top banks offering franchise loans include:

- Wells Fargo

- Chase Bank

- Bank of America

- Live Oak Bank

- TD Bank

Each bank has its own loan products and terms. It helps to compare offers before choosing.

Sba Loans

Types of SBA Loans for Franchises include 7(a) loans, CDC/504 loans, and microloans. The 7(a) loan is the most common and offers up to $5 million. CDC/504 loans help with fixed assets like real estate. Microloans provide smaller funds for startups or small needs.

Application Process usually requires a solid business plan, financial statements, and good credit. The SBA works with approved lenders, so applying happens through banks or credit unions. Approval times vary but often take a few weeks to months.

Advantages include lower down payments, longer repayment terms, and competitive interest rates. SBA loans also offer support from the government, which lowers lender risk. Limitations include strict eligibility rules, detailed paperwork, and a slower approval process compared to other loans.

Alternative Lenders

Online lenders and platforms offer quick access to funds. They use simple applications and fast approval processes. Many provide flexible loan amounts suited for franchises. Borrowers can often get money within a few days. These lenders usually have less strict requirements than banks.

Fast funding solutions help franchises start or grow without delay. Some lenders provide same-day or next-day funding options. This speed helps meet urgent business needs. It also allows franchisees to seize timely opportunities.

| Interest Rates | Loan Terms |

|---|---|

| Can be higher than traditional banks | Often shorter, from 6 months to 5 years |

| May vary based on credit and business history | Repayment schedules can be weekly or monthly |

| Some lenders offer fixed or variable rates | Terms may include prepayment options without penalty |

Personal Funding Options

Using personal assets means using your savings, home equity, or investments to fund your franchise. This method avoids loan approval processes but puts your own money at risk. It can be faster but might limit your cash flow.

Borrowing from friends and family can be easier and may have flexible terms. Trust is key, and clear agreements help avoid misunderstandings. Always treat it like a business deal to keep relationships strong.

Risks and considerations include losing personal assets or damaging relationships if repayments are missed. Both options require careful planning and honesty about your ability to repay. Think about these risks before deciding.

Choosing The Right Lender

Assessing funding needs helps decide the loan amount required. Consider costs like franchise fees, equipment, and working capital. Know your budget limits to avoid borrowing too much.

Comparing loan terms is key. Check interest rates, repayment periods, and fees. Shorter terms mean higher monthly payments but less interest overall. Longer terms lower payments but increase total cost.

Evaluating lender reputation ensures trust and support. Research online reviews and ask other franchise owners about their experiences. A good lender offers clear communication and fair policies.

Tips For Fast Loan Approval

Prepare all necessary documents before applying for a franchise loan. This includes business plans, financial statements, and tax returns. Having these ready can speed up the approval process.

Improve your credit profile by paying bills on time and reducing debts. A higher credit score often leads to better loan terms and faster approval.

Work closely with loan specialists who understand franchise financing. They can guide you through options and help avoid common mistakes.

Frequently Asked Questions

What Is The Best Loan For A Franchise?

The best loan for a franchise is typically an SBA loan due to low interest rates and favorable terms. Banks and franchisor financing also work well. Choose based on your credit, franchise type, and funding needs for optimal results.

Will Banks Give Loans For Franchises?

Yes, many banks offer loans for franchises through SBA-backed, commercial, or specialized franchise financing programs.

How To Get A Loan For A Franchise?

Apply for a franchise loan by researching lenders, preparing a solid business plan, and choosing SBA, bank, or franchisor financing options.

What Is The Monthly Payment On A $50,000 Business Loan?

Monthly payments on a $50,000 business loan vary by interest rate and term length. For example, a 5% rate over 5 years costs about $943 monthly. Use a loan calculator to get precise amounts based on your specific loan terms and lender conditions.

Conclusion

Choosing the right lender makes a big difference for your franchise success. Compare loan types carefully before deciding. SBA loans often offer lower rates and longer terms. Banks provide strong support but may require solid credit. Alternative lenders can be faster but cost more.

Franchisor financing might include special perks for new owners. Use personal savings only if comfortable with the risk. Research each option to find what fits your needs best. Taking time now helps avoid problems later. Your franchise dream deserves thoughtful planning and smart financing.