Are you curious about how lenders check your credit without hurting your score? That’s where a Soft Inquiry Lender Precheck comes in.

It’s a simple, risk-free way for you to see if you qualify for loans or credit offers without any negative impact on your credit report. Imagine getting a sneak peek at your chances before fully committing—wouldn’t that give you peace of mind?

You’ll discover exactly what a soft inquiry is, how it works, and why it matters to your financial future. Keep reading to take control of your credit journey with confidence.

Soft Inquiry Basics

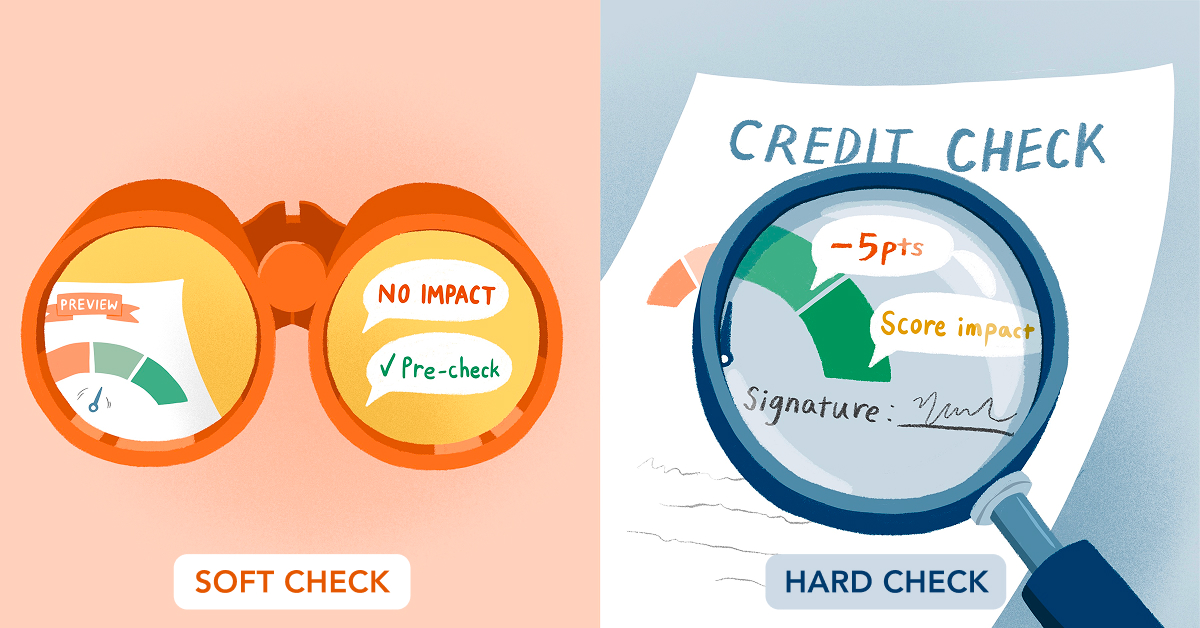

A soft inquiry is a credit check that does not affect your credit score. It happens when you or a lender looks at your credit report without your full application. This is also called a soft pull.

In contrast, a hard pull occurs when you apply for credit, like a loan or credit card. Hard pulls can lower your credit score slightly. Soft inquiries do not.

Soft inquiries occur in many cases:

- Checking your own credit report

- Pre-approval offers from lenders

- Background checks by employers

- Lenders doing a quick check before loan approval

Soft inquiries help lenders see your creditworthiness without affecting your score. They are less intrusive than hard pulls.

Lender Precheck Process

Soft inquiries let lenders check credit without hurting your score. They use this to see if you qualify before giving a loan offer. This step is called pre-approval. It helps lenders decide if they want to move forward with a full credit check.

Soft pulls show basic credit info, not the full report. They do not affect your credit score. Many people confuse soft inquiries with hard inquiries, but only hard ones lower your score.

Soft inquiries are common when you ask for pre-approval on a loan or credit card. They help lenders make quick decisions without risking your credit health.

Impact On Credit Scores

Soft inquiries happen when a lender or you check your credit report. These checks do not lower your credit score. Unlike hard inquiries, soft pulls are just for pre-approval or personal review.

Avoiding score damage is easy by choosing lenders who use soft inquiries. These checks let you explore loan offers without risk. Make sure to confirm the type of inquiry before proceeding.

Regular monitoring of soft inquiry activity helps you spot any unusual checks. You can review your credit reports for free once a year from major bureaus. This keeps your credit information safe and accurate.

Benefits Of Soft Inquiry Prechecks

Soft inquiry prechecks help lenders decide quickly if you qualify. They show your credit info without affecting your credit score. This boosts approval chances because lenders see your creditworthiness early. Faster decisions mean less waiting and stress for you.

Soft inquiries let lenders avoid unnecessary hard pulls. Hard pulls can lower your credit score if done too often. Reducing hard pulls keeps your credit healthier. It also means fewer rejections due to multiple credit checks.

Overall, soft inquiry prechecks offer a simple way to check eligibility. They save time and protect your credit score. This helps you apply with more confidence and less risk.

Smart Strategies For Borrowers

Checking your own credit with soft pulls helps keep your credit score safe. These checks do not affect your score and let you see your credit health anytime. It’s smart to review your credit before applying for loans.

Choosing lenders that use soft checks means fewer hard inquiries on your report. Soft checks allow you to get pre-approved or check offers without hurting your credit. Always ask lenders if they use soft or hard pulls first.

Preparing for hard inquiries is key before applying for credit. Multiple hard inquiries can lower your credit score. Keep your loan applications close together to limit damage. Track your inquiries and only apply when ready.

Tools And Resources

Credit monitoring services help track your credit score regularly. They show changes and alert you to unusual activity quickly. Many services offer free reports and tips to improve credit health.

Loan rate prechecks let you see potential loan offers without hurting your credit score. These soft inquiries help compare rates from different lenders safely. You can find the best deal before officially applying.

Educational platforms provide easy lessons about credit and loans. They explain terms and processes in simple words. These resources help users make smart financial decisions and avoid common mistakes.

Frequently Asked Questions

What Do Lenders See On A Soft Inquiry?

Lenders see your credit score, credit limits, and recent account activity during a soft inquiry. It does not affect your credit score.

How Rare Is An 830 Fico Score?

An 830 FICO score is extremely rare, placing you in the top 1% of consumers. It reflects exceptional credit management and reliability.

Are Pre-approval Soft Inquiries?

Pre-approval usually involves a soft inquiry, which does not affect your credit score. Lenders use it to check your creditworthiness.

What Kind Of Credit Score Do You Need To Buy A $300,000 House?

You typically need a credit score of 620 or higher to buy a $300,000 house. Higher scores get better rates.

Conclusion

Soft inquiry lender prechecks help you understand loan options without credit damage. They offer a risk-free way to see potential loan terms. You stay in control of your credit health while exploring choices. Knowing this process can make borrowing simpler and less stressful.

Always check with lenders about the type of credit pull they use. This small step protects your score and keeps your finances strong. Soft inquiries provide useful insight without lowering your credit rating. Use them wisely to make smarter financial decisions.